Mortgage vs rent—man, that’s been haunting me lately. Like, seriously, here I am on Christmas Eve 2025, sitting in my rented apartment in the Midwest, staring out at the snowy street while the heater rattles like it’s judging me, and I’m still flipping back and forth on whether buying a house would’ve been smarter or if renting is saving my butt right now.

I gotta be real with you—I’ve rented for the last eight years straight, ever since that disaster in 2018 when I almost bought a fixer-upper in Denver. Oh god, that story. I was so hyped, put in an offer on this cute but totally rundown bungalow, got approved for a mortgage at like 4% rates (which felt high then, ha!), and then the inspection came back with foundation issues that would’ve cost me 50k to fix. I backed out, lost my earnest money, and felt like the biggest idiot. Anyway, fast-forward to now, and mortgage vs rent feels even more loaded with rates dipping to around 6% but home prices still crazy high.

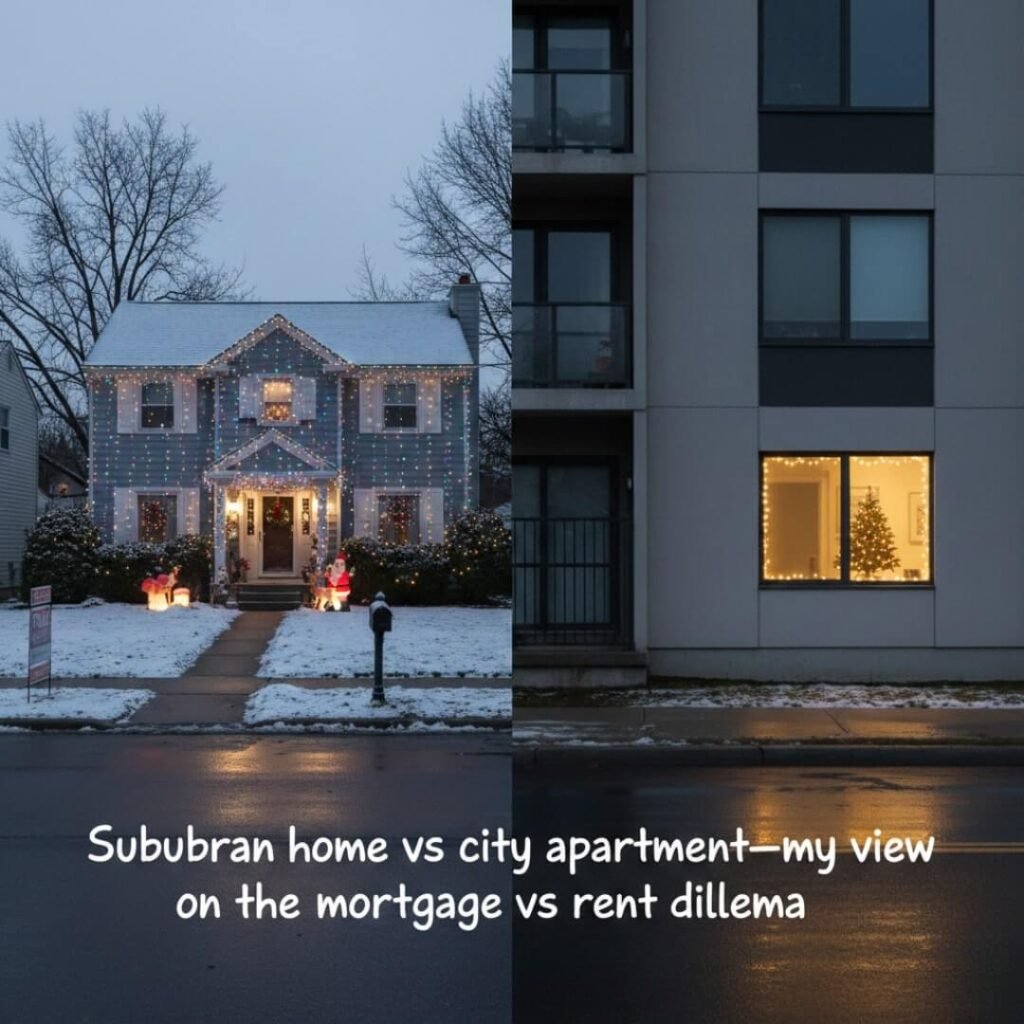

Why Mortgage vs Rent Feels So Personal Right Now

Look, in 2025, the numbers are wild. Average home prices are hovering around $410,000-$430,000 nationally, mortgage rates for a 30-year fixed are about 6%, and that means monthly payments (with taxes, insurance, all that jazz) can hit $2,500 or more easy. Meanwhile, average rent is like $1,700-$2,000 depending on where you are. I’ve been paying $1,800 for my two-bedroom here, and yeah, it’s gone up a bit each year, but nothing like the horror stories from friends who bought and now deal with surprise repairs.

But here’s the contradiction that’s messing with my head: long-term, buying builds equity, right? Like, if I could’ve stuck it out, that Denver house might be worth double now. Yet right now, studies are saying renting is cheaper monthly in most big metros—Bankrate found it’s more affordable to rent than own in all 50 largest markets this year. Investopedia even crunched it and said renting can save $400 a month in high-rate environments. Me? I invested the money I didn’t put into a down payment, and it’s grown okay, but not amazing.

The Raw Pros and Cons of Mortgage vs Rent From My Flawed Experience

Okay, let’s break it down like I’m chatting with you over bad holiday coffee.

Pros of Buying (Why I Sometimes Regret Not Pulling the Trigger)

- You build equity, dude. Every payment chips away at the principal, and if prices appreciate (they’ve slowed but still up a bit), you win big.

- Fixed payments mostly—my friends with mortgages locked in lower rates years ago are laughing while rents spike.

- Freedom to paint walls weird colors or whatever. I once got dinged on my deposit for “unauthorized” shelves. Embarrassing.

Cons of Buying (Why I’m Kinda Glad I Dodged It)

- Upfront costs are brutal—20% down on a $400k house? That’s 80 grand I don’t have lying around.

- Maintenance. My buddy just dropped 10k on a new roof. Me? Landlord fixes the leaky faucet, even if it takes forever.

- Rates at 6% make monthly costs higher than rent in a lot of places right now.

Pros of Renting (My Current Reality)

- Flexibility—like, if I hate the noisy neighbors (current situation, ugh), I can move without selling.

- Lower monthly in 2025 for many spots. Seriously, check a rent vs buy calculator like the NYT one; it often tips toward renting short-term.

- No property taxes or HOA drama eating your soul.

Cons of Renting (The Stuff That Keeps Me Up)

- Rent goes up. Mine jumped 10% last renewal.

- No equity. Feels like throwing money away sometimes, even if the math says otherwise right now.

- Landlords. Mine’s okay, but stories from friends… yikes.

My Biggest Mortgage vs Rent Mistakes (So You Don’t Repeat Them)

I once ran the numbers wrong and thought buying was always better—ignored opportunity cost. If you rent and invest the difference, it can beat buying, especially with rates like this. Use tools like NerdWallet’s rent vs buy calculator; plug in your numbers. For me, staying 5+ years tips toward buying, but under that? Rent.

Another oops: I underestimated moving costs both ways. Renting means more frequent moves sometimes, and that’s expensive.

Wrapping This Mortgage vs Rent Ramble Up

Honestly? Mortgage vs rent doesn’t have a one-size answer. For me right now, in this weird 2025 market with rates cooling but prices stubborn, renting feels smarter—gives me breathing room while I figure out if I wanna stay put. But if you’re planning 10+ years and can swing the down payment without raiding emergencies, buying might build that wealth.

Anyway, run your own numbers, talk to a non-pushy advisor, and whatever you pick, don’t beat yourself up—like I still do over that Denver flop. What’s your take? Drop a comment if you’re debating mortgage vs rent too. Happy holidays, y’all—here’s to smarter choices in 2026.

(References: Data pulled from sources like Bankrate’s 2025 Rent vs. Buy study [https://www.bankrate.com/real-estate/rent-vs-buy-affordability-study/], Investopedia [https://www.investopedia.com/deciding-between-renting-and-buying-in-2025-one-choice-saves-usd400-monthly-11809281], and NYT Rent vs. Buy Calculator [https://www.nytimes.com/interactive/2024/upshot/buy-rent-calculator.html] for credibility.)

{kind=link}