Look, retirement planning isn’t some perfect science. I remember back in my 30s, thinking I’d be set with whatever was in my 401(k), but then life hit—kids, a house that needed way more repairs than expected, that embarrassing period where I yolo’d into some meme stocks and lost a chunk. Anyway, fast forward to now, mid-50s, and I’m staring at spreadsheets wondering if I’ll ever chill on a beach without checking my balance app every five minutes. The truth? Most Americans think you need around $1.26 million to retire comfortably these days, according to that Northwestern Mutual study from earlier this year. But honestly, for me, that number feels both too high and too low at the same time—like, will it cover healthcare surprises?

How Much Money Do You Really Need? Breaking Down the Numbers

Okay, let’s get real about how much money to retire. Experts like Fidelity say aim for 10x your final salary by age 67. So if you’re pulling in $100k a year toward the end, that’s a million bucks. But I kinda contradict myself here because sometimes I think, man, if I downsize and move somewhere cheaper, maybe half that? Studies show it varies wildly by state—over $2 million in Hawaii, but under $800k in places like West Virginia. Me? I’m in Illinois, so probably somewhere in the middle, but inflation’s been a beast lately.

The classic 4% rule says withdraw 4% of your nest egg the first year, adjust for inflation after. So $1 million gives you $40k a year, plus Social Security. But with markets being wild, some folks are bumping it to 4.7% now. I tried a few online retirement calculators—like Vanguard’s or Fidelity’s—and plugged in my numbers. Shocking revelation: I was way behind at 50, but ramping up contributions caught me up-ish.

My Biggest Retirement Planning Mistakes (So You Don’t Repeat ‘Em)

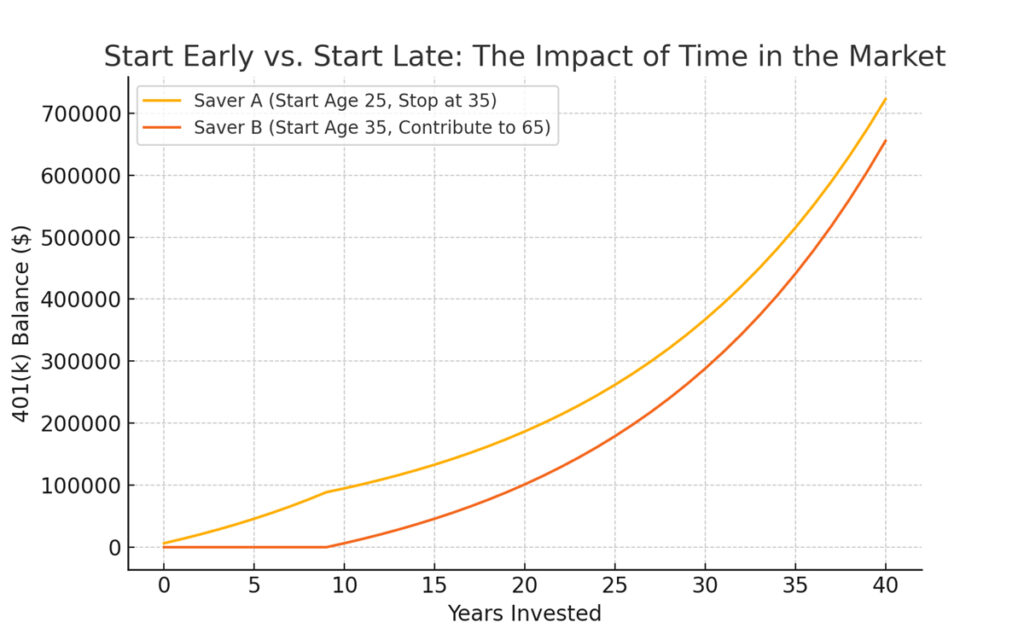

- Starting too late: I didn’t max my 401(k) until my 40s. Compound interest is magic, y’all—starting at 25 vs. 35 is night and day.

- Ignoring healthcare: Thought Medicare would cover everything. Nope. Fidelity estimates $172k just for that in retirement.

- Panicking during dips: Sold low in 2022, bought high later. Classic me.

- Not diversifying enough: Too heavy in tech stocks for a while. Ouch.

Here’s what helped turn it around:

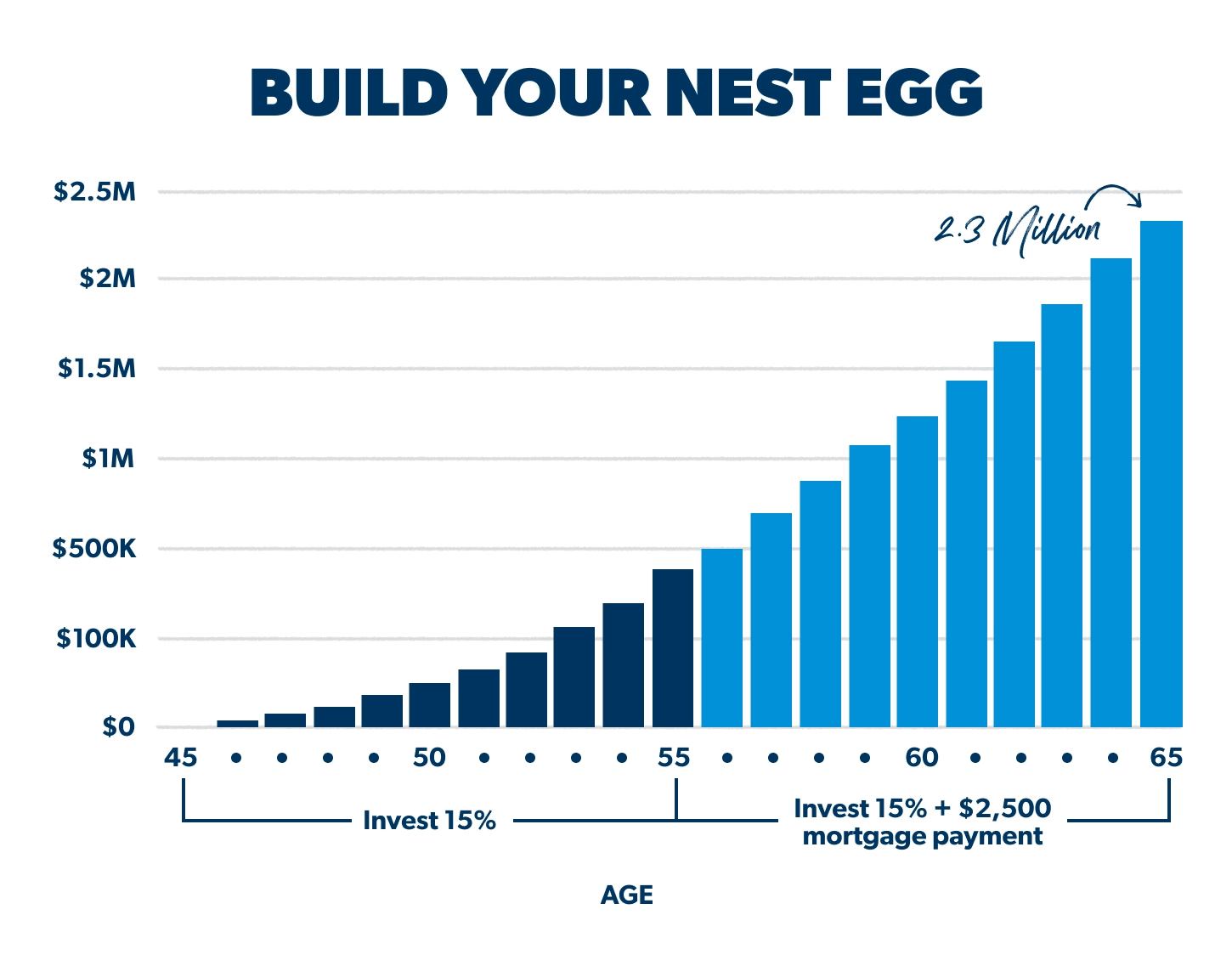

- Save 15% of income if you can (Fidelity’s guideline).

- Use catch-up contributions if over 50.

- Run scenarios on a good retirement calculator.

Dreaming Big: What Retirement Planning Could Look Like If You Nail It

If I hit my numbers, I see us traveling—not fancy cruises, but quirky road trips, maybe renting an RV and hitting weird roadside attractions. Or just relaxing with grandkids. But seriously, retirement planning made simple boils down to knowing your “enough” and building toward it without perfection.

Wrapping This Up Like a Late-Night Chat

Anyway, rambling over—retirement planning is personal, flawed, and ongoing for me. How much money do you really need to retire? Whatever lets you sleep without worry, plus a buffer for surprises. My advice? Plug your info into a free tool like Vanguard’s retirement income calculator or Fidelity’s. Talk to a fiduciary advisor if it gets overwhelming. Start small today, forgive past mistakes (like I try to), and keep going. You’ve got this—or at least, we’re in it together. Happy holidays, and here’s to better numbers in 2026! What about you—what’s your biggest retirement worry right now? Drop a comment.

{kind=link}