Tax planning to legally reduce my tax bill is something I’ve been obsessing over lately, seriously. Like, here I am on Christmas Eve 2025, sitting in my chilly living room in suburban Chicago—fireplace crackling, snow piling up outside, kids finally asleep after way too much sugar—and I’m crunching numbers instead of wrapping the last gifts. Pathetic, right? But honestly, after getting slammed with a bigger bill than expected last year, I swore I’d get smarter about this stuff. Anyway, I’m no expert, just a regular dude who’s made some dumb mistakes and learned a few tricks to legally lower taxes without getting in trouble with the IRS.

Why Tax Planning to Legally Reduce Your Tax Bill Actually Matters to Me

Look, I used to ignore all this. Filed my taxes last minute every year, took the standard deduction, and grumbled when the refund was tiny or—worse—I owed money. Then 2024 hit, and boom, unexpected freelance income pushed me into a higher bracket. I ended up owing thousands, and it stung bad. Like, had to dip into savings meant for a family vacation. Embarrassing, yeah. But it lit a fire under me. Now, with these new rules from that big tax bill earlier this year, there are legit ways to shave down what you owe. And trust me, legally reducing your tax bill feels pretty damn good. Tax Planning Guide

Americans have the ‘tax scaries’—but good news is waiting as the …

[Insert placeholder: Stressed person at desk] Image Details: A candid, slightly off-center shot of me (or someone like me) hunched over a laptop with tax software open, forehead in hand, surrounded by crumpled receipts and a cold coffee mug—personal perspective showing the real frustration before the “aha” moments, with alt text: “Me stressing over taxes before figuring out better planning.”

My Go-To Moves for Tax Planning to Legally Reduce My Tax Bill: Retirement Contributions

Okay, the biggest win for me this year? Maxing out retirement accounts. I finally bumped up my 401(k) contributions at work—up to that $23,500 limit for 2025. It hurts a bit seeing the paycheck smaller, but man, it directly lowers your taxable income right now. Pre-tax dollars, baby. And my employer matches some of it, so free money. I also threw some into a traditional IRA. Sensory detail: I remember sitting at the kitchen table last January, hot coffee steaming, logging into the portal and cranking that percentage up. Felt scary, but now? Cautiously optimistic.

- 401(k) or similar: Contribute pre-tax, lowers your bill immediately.

- IRA (traditional): Up to $7,000 if under 50—deductible if you qualify.

- Roth options: I did a little Roth too, ’cause tax-free later might be huge if rates go up.

Pro tip from my screw-up: Don’t forget catch-up if you’re over 50. I wish I qualified already.

Piggy Bank With 401 Vs Ira Individual Retirement Accounts Written …

[Insert placeholder: Piggy bank retirement] Image Details: Close-up from my viewpoint of two piggy banks labeled “401k” and “IRA” on a windowsill with snow outside, one overflowing with coins to show growth—slightly unusual angle looking down, personal and hopeful, alt text: “My retirement savings starting to stack up thanks to better tax planning.”

For more on retirement limits, check out the IRS site. Tax Planning Guide

How Charitable Donations Helped Me Legally Reduce My Tax Bill Tax Planning Guide

This one surprised me. I’ve always donated here and there—old clothes to Goodwill, some cash to local food banks—but I never tracked it properly. This year, with itemizing making more sense (thanks to higher SALT caps now), I bunched donations. Gave a bigger chunk to my favorite charity in December. Felt good helping people, and yeah, it knocked down my taxable income. Slightly embarrassing story: I almost forgot to get receipts for everything, nearly missed out on the deduction. Lesson learned.

If you itemize:

- Cash donations up to certain limits.

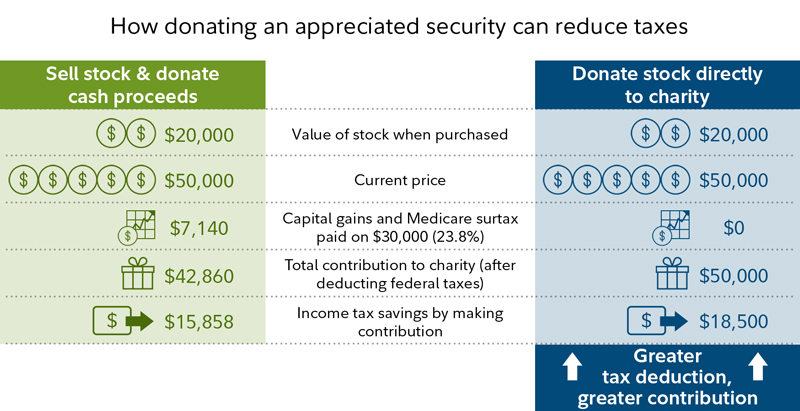

- Appreciated stock—even better, avoids capital gains tax.

Charitable giving and taxes | Fidelity Tax Planning Guide

Fidelity has good info on charitable giving strategies. Tax Planning Guide

Other Random Tax Planning Tricks I’ve Tried to Legally Reduce My Tax Bill

- Harvest losses: Sold some loser stocks to offset gains. Painful but saved me on capital gains tax.

- HSA if eligible: Triple tax win—pre-tax in, grows tax-free, out tax-free for medical.

- Standard vs. itemize: This year, with new rules, itemizing edged out for me thanks to property taxes.

And hey, energy credits or whatever if you went green—didn’t apply to me, but worth checking.

Wrapping This Up: My Take on Tax Planning to Legally Reduce Your Tax Bill

Alright, rambling over. Tax planning isn’t sexy, and I’ve contradicted myself plenty—hated cutting my paycheck short at first, but now I’m hooked on seeing that lower bill projection. It’s flawed, it’s human, but it works. If you’re like me, procrastinating in your PJs on Christmas Eve, just start small. Talk to a pro if you can afford it, or dig into IRS.gov yourself.

Call to action: Pick one thing—like bumping your 401(k)—and do it today. Seriously, future you will thank present you. Merry Christmas, and here’s to smaller tax bills in 2026.

Financial Tax Planning Desk Scene with Coins Documents Stock …

{kind=link}